By Raphaël Rauner

As the Russo-Ukrainian conflict intensifies, the global geopolitical narrative is shifting. It impacts every actor on the world stage- from small to large. It also raises questions about New Zealand’s place in the world and our dependence on international partners. This article is not about foreign policy. It’s about New Zealand’s fuel resilience and future without an oil refinery.

This fuel resilience issue arose in August 2021 when Refining NZ decided to close the Marsden Point Oil Refinery for cost reasons. The ensuing months saw the Cabinet’s refusal to intervene and keep the refinery operating (RNZ, 2021). The result were questions about our fuel resilience and energy security- since this policy deepens our dependency on partners in the Middle East and Australasia for refined fuels.

A Glance at Our Current Fuel Infrastructure

Even as we shift toward green alternatives, the Black Gold runs everything- from transportation to the clothes on our backs. For the past 61 years, this substance has been discharged by large oil tankers at Marsden Point, a nook on Whangārei Harbour. There, crude oil becomes refined fuel: petrol, kerosene, and diesel. The refinery also supplements bitumen and farming fertilisers.

The refined product makes its way to the local gas station through pipelines and other transit methods. A vital pitstop is the reserves at Wiri Terminal, South Auckland- an essential infrastructure for New Zealand’s fuel supply (sharechat.co.nz, 2022). These reserves contain around 64 million barrels- or one year’s worth of fuel at current consumption rates (Newsroom, 2022). However, some question whether this is enough?

That question continues to define the tug-of-war between the Government and energy security experts. On the one hand, the Ministry of Business, Innovation, and Employment argued in a Cabinet paper titled Fuel Resilience without a Domestic Refinery that a ‘no fuel’ scenario is implausible and that a domestic refinery would not make a difference. Their reasoning is New Zealand’s existing dependence on crude oil imports- 30% of which is refined before arrival (NZ Herald, 2012).

On the other side, energy security experts argue that global winds are shifting- underscored with the current conflict in Ukraine- and its impacts on the international fuel markets. Some say that international instability may disrupt our supply chain and force us to seek new partnerships (Newsroom, 2021). They also argue that the refinery is “one of the country’s most important tools for supply shortages”- A claim that Refining NZ denies by noting that New Zealand currently does not produce crude oil.

A Dependence on International Partners

Having assessed the domestic aspect of the fuel resilience issue, much of the concern lies on the international stage. Partners such as Russia, the Middle East, Singapore and South Korea build New Zealand’s intricate network of suppliers.

New Zealand’s continued flow of the Black Gold is also supported by a series of carefully orchestrated institutions and bilateral agreements. The most renowned institution that safeguards New Zealand’s interests is the International Energy Alliance (IEA). The IEA gives fuel importing countries (like New Zealand) leverage over fuel prices and supply (iea.org, 2022). The IEA has also provided guidance over energy policy matters to countries; however, its role has been significant in ensuring continued supply since the 1973 Arab Oil Crisis (Samuelson, 2008).

In addition to strong IEA participation, the government has also entered bilateral agreements with the Netherlands, United Kingdom, Australia, and Japan to ensure supply in an emergency (Samuelson, 2008). However, fissures can emerge in our ties with these ‘allies’ as interests and relationships change. Changes in these relationships have arisen throughout recent years as New Zealand has pursued foreign policy stances that do not cohere with some of those partners; the most notable example was New Zealand’s decision not to participate in AUKUS.

A Supply Vulnerable to Attack

If there’s one lesson to be learnt, it is that bilateral ties do not safeguard New Zealand’s fuel supply from global instability. Several events in recent history are a testament to New Zealand’s precarious energy supply as global ‘shocks’ often impact Kiwi consumers within hours. The war in Ukraine is one clear example as its implications are felt strongly by Kiwi consumers, who are now paying record prices at the pump. However, these ‘shocks’ can happen suddenly, as the 2019 Saudi Oil Field Attacks underlined the vulnerability of the global fuel supply (NZ Herald, 2019). However, these attacks were short and sharp, as the Saudi Government restored total refining capacity within days.

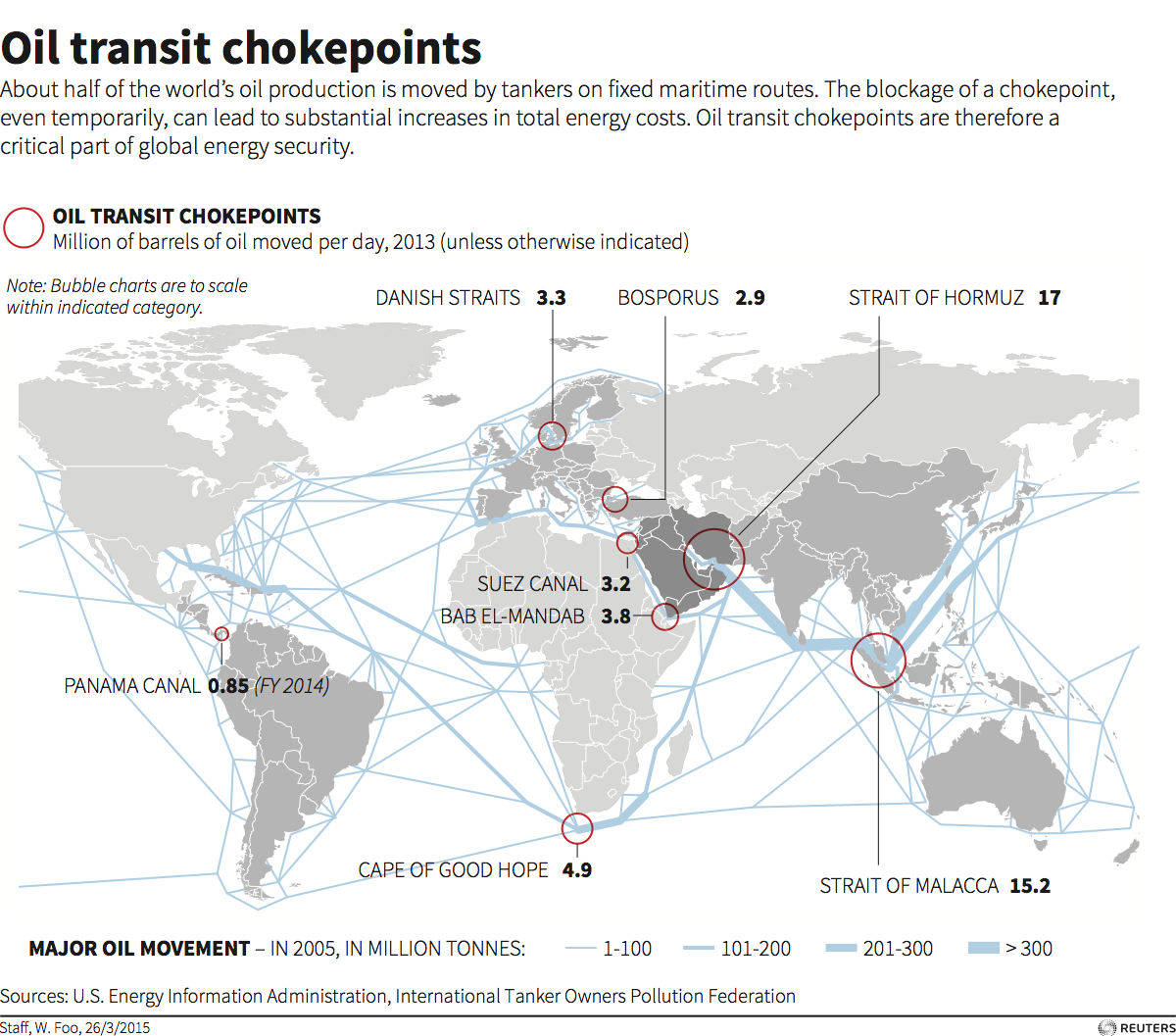

As these events show, the global geopolitical landscape’s unpredictability does raise questions about New Zealand’s fuel security, especially in the South China Sea and surrounding areas (Newsroom, 2019). These concerns align strongly with chokepoints in the global oil supply and the location of refineries that will now sustain New Zealand (Visual Capitalist, 2021).

One relevant area of concern is the Strait of Malacca (in Southeast Asia), which sees 61% of the world’s oil supplies travel through the area before refining in Singapore. This area will now be more critical than before as our refined fuels will originate from Southeast Asian partners. It also means political changes in the region will have a strong bearing on how Kiwis will live their lives, significantly if choke points are compromised, and refining infrastructure is ever besieged. However, the Malacca Strait is only one choke point among many in world supply chains.

Final Remarks

While fuel resilience is a topic filled with complexity, the article discussed the precarity of Black Gold. The journey from the oil field to the pump is a long, complex, and difficult road. In these times, it is also heavily influenced by international politics and the relationships New Zealand fosters. However, we’re not alone. Disruptions impact everyone similarly, and recent events are a testament to this. Do we need to consider the future without a refinery and our increasing dependence on refined fuels from our overseas partners? Are we safe from geopolitical shifts? Do we need to increase our reserves? Should we foster new bilateral ties?

Bibliography

- https://www.mbie.govt.nz/assets/77e0694e33/oil-an-introduction-for-new-zealanders.pdf

- https://www.visualcapitalist.com/mapping-the-worlds-key-maritime-choke-points/

- https://www.eia.gov/todayinenergy/detail.php?id=32452

- https://www.rnz.co.nz/news/business/457607/fuel-experts-divided-on-impact-of-marsden-point-refinery-closure

- https://www.newsroom.co.nz/russia-ukraine-war-changes-fundamentals-on-nz-fuel-supplies

- https://www.mbie.govt.nz/dmsdocument/17736-fuel-supply-resilience-without-a-domestic-oil-refinery-minute-of-decision-proactiverelease-pdf

- https://www.iea.org/about

- http://www.sharechat.co.nz/article/3f5003dc/wiri-terminal-alternative-wouldn-t-have-avoided-pipeline-woes-mbie.html

- https://www.nzherald.co.nz/business/saudi-arabia-attacks-our-petrol-prices-could-rise-by-10c-a-litre/ELO3PABU7A2SM7XNXAEDL2OJLQ/

- Picture

- https://unitedcivil.co.nz/services/industrial-infrastructure/

- https://www.visualcapitalist.com/mapping-the-worlds-key-maritime-choke-points/

- https://www.businessinsider.com.au/worlds-eight-oil-chokepoints-2015-4?r=US&IR=T